RunRox - Advanced SMC⭐️ Introducing Our Advanced SMC Indicator: Elevate Your Smart Money Concept Trading

We are excited to present our innovative indicator, specifically designed for the Smart Money Concept (SMC). Our approach goes beyond the traditional SMC strategy by offering significant enhancements that can help you achieve stronger trading performance.

We employ a more sophisticated SMC structure, incorporating improved IDM (Inducement) logic, both internal and external structures, and four types of order blocks. This allows for deeper insights into market trends and a clearer understanding of how major market participants may be manipulating price action.

🟠 Indicator Features:

Structure

HTF Structure – Choose any timeframe and display its structure on your current chart.

CHoCH | BOS | IDM – Display any components from this structure.

Market Minor Structure – Swing and Minor structure.

BOS/CHoCH Breaking by (Body | Wick) – Choose the principle for building the structure, either by the candle body or by their wicks.

BOS/CHoCH Move if Swept – When liquidity is taken, decide whether to move the structure line higher or consider it a structural break.

Move CHoCH/BOS – Relocate key points on the chart if the structure becomes too large.

FVG Concept

HTF FVG – Choose any timeframe from which you want to display FVG on your current chart

Three Types of FVG – Classic FVG, Double FVG, Implied Imbalance

Reaction to FVG – Show the market’s reaction to FVG on the chart

Mitigation Method – Select the fill method that suits your approach (Touch/Midline/Complete)

Remove Filled FVG – Remove FVGs from the chart once they have been filled

Combine FVG – Merge several consecutive FVGs into one

Length FVG – Adjust the number of candles that define the FVG

OrderBlock Concept

HTF OrderBlock – Choose any timeframe from which you want to display orderblocks on your current chart

Swing and Minor Orderblocks – Display only the orderblocks you need, whether from the Swing or Minor structure

Four Types of Order Blocks – Advanced OB, Classic OB, BTS/STB zones, Extremum Candle

Block Based on – Decide whether to base the orderblock on candle highs/lows or candle open/close

Mitigation Method – Define when an orderblock is considered filled (Touch/Midline/Complete)

Remove Blocks Older – Remove older orderblocks from the chart

Hide Overlap – Disable overlapping orderblocks when they appear in the same area

Eat Young Blocks – Reduce the size of an orderblock until it fully forms

Hide Distant Blocks – Remove orderblocks that are too far from the current price

Previous Highs & Lows

Four Level Types – Day, Week, Month, Quarter

Style Customization – Choose line color, line style, and transparency

Fibonacci Retracements

10 Template Options – Ten different bases on which you can build your Fibonacci grid

Up to 7 Levels – Add up to seven Fibonacci levels for your convenience

Fibo Inversion – Option to invert the Fibonacci grid

Style Customization – Choose line colors, line styles, and transparency

Additional Functions

Premium & Discount Zones – A popular concept we’ve incorporated to help identify potential trading areas within premium or discount prices

Equal Highs & Lows – High-liquidity levels where market makers may seek liquidity

Color Candles – Automatically colors candles based on the current trend

Market Structure ZigZag – Offers a clear visual of the zigzag pattern on which the structure is built

Key Point Labels – Displays important swing high/low points directly on the chart

General Styling – Customize any chart element, including size, style, color, and transparency

Alert Customization – Over 16 types of alerts, easily configured in a few clicks. Receive only the notifications you need. Custom alerts are also available for developers.

Next, we will provide a detailed overview of all the indicator’s features, accompanied by chart examples.

📈 Structure

What Is IDM?

IDM, or the Institutional Distribution Model, is an advanced concept within SMC that focuses on how institutional players distribute their positions in the market. By analyzing IDM, traders can better anticipate price movements and potential turning points, thereby gaining a meaningful edge in their trading.

In our structure concept, IDM can form under specific conditions. The market does not always provide a high-liquidity point to work with, so we’ve adopted a flexible approach. We generate IDM when a certain type of liquidity appears during the impulse and BOS break, allowing for a potential future liquidity sweep.

Below, I will provide an example that illustrates when IDM forms as a liquidity magnet within the structure - and when it does not.

As shown in the example above, we focus on the initial impulse after the BOS. If liquidity forms during this impulse - liquidity that needs to be taken out during the structural move - we mark an IDM level as a price magnet. However, if this liquidity does not appear, we do not create an IDM. In that case, the same point might serve as an FVG or play a different role, depending on your trading approach.

This concept makes the structure more flexible and better able to respond immediately to market movements and key structural points.

Above is an example on the chart illustrating what the structure looks like both with and without IDM. As you can see, when the structural move includes pullbacks and consolidation, there is an opportunity to form an IDM as a price magnet. However, if the impulses are strong and lack pullbacks, FVG becomes the only magnet in that move. Depending on the chart, our indicator adapts to the current market conditions and highlights potential liquidity collection points.

📊 Swing and Minor Structure

In the new version of the indicator, the minor structure and the swing structure differ from each other.

Swing structure - In this structure, as mentioned earlier, the IDM concept remains a price magnet and is formed at certain points on the chart if the conditions allow. If these points do not appear, IDM might not form at all.

Minor structure - Here, we have completely removed IDM and only kept BOS and CHoCH for structure formation. We found that for a minor structure, this approach allows faster reactions to trend changes, depending on market movements.

By making these adjustments, we have resolved the main issue of the advanced structure, which was the large distance between BOS and CHoCH that sometimes resulted in a month-long consolidation between these levels. In this version, those problems no longer occur.

If, for some reason, your settings result in a larger swing structure, you can still work with the minor structure using the same POI as in the swing structure. OrderBlock and FVG remain the primary drivers of order flow.

Shown above is a screenshot of the main structure settings you can adjust. These settings are highly flexible and can be tailored to fit a wide range of trading preferences.

⚖️ FVG Concept

A new feature of our indicator is the FVG concept. We automatically detect three types of FVG at the moment, which will be explained below.

FVG - the standard Fair Value Gap

Double FVG - a double FVG, also referred to as BPR (Balanced Price Range)

Implied Imbalance - a type of imbalance that arises from buyer or seller demand

Below, we will look at examples of the FVG types we currently identify.

All price inefficiencies work in real time, immediately appearing on the chart and allowing traders to quickly respond to FVG reactions.

We have also enhanced this concept by displaying FVG reactions on the chart. If an FVG triggers a reaction and the price responds to that range, we highlight it on the chart, so you can recognize the reaction and make timely trading decisions. A screenshot below shows how this looks in practice.

Below is a screenshot illustrating the main settings of this concept, along with detailed descriptions.

📦 OrderBlock Concept

OrderBlocks provide an effective way to identify areas of interest and make informed decisions. We have dedicated significant effort to refining this section’s functionality and have achieved strong results in doing so.

Order Block Types

Advanced OrderBlock – A specialized type of order block generated by our internal algorithm. This can help traders aim for tighter entries and potentially more favorable risk-reward ratios within a narrow price range.

OrderBlock – The classic type, formed at the highs or lows of a structure when a BOS or CHoCH occurs. It can still be an effective entry method but typically spans a wider price range.

Extremum Candle – Based on liquidity grabs. The candle creating this order block must collect liquidity before making an impulsive move that breaks the BOS or CHoCH.

BTS / STB (Buy To Sell / Sell To Buy) – This concept may appear when market makers manipulate price to buy or sell an asset. It often covers a larger price range because it relies on a brief impulsive move to form.

Each type of order block has its own strengths and weaknesses. We provide traders with the flexibility to choose which types suit their trading style and preferences.

Above is an example of how you can apply OrderFlow alongside our structure and orderblocks, which can produce solid results when combined with the Smart Money concept.

In this demonstration, we have highlighted the Advanced Orderblock as an illustration.

Above is a screenshot of all the settings related to this section. They can be customized to suit your specific needs, ensuring you only see what is genuinely relevant on your chart.

📏 Previous Highs and Lows

You can select four levels to display on the chart as some of the most liquid zones:

Daily Highs and Lows

Weekly Highs and Lows

Monthly Highs and Lows

Quarterly Highs and Lows

This feature helps you identify important levels on lower timeframes and focus on these zones for potential trading opportunities. Below is an example of how it appears on the chart.

Below, you can see the settings available in this section.

📐 Fibonacci Levels

Likewise, a new section in our indicator is Fibonacci Levels, a well-known tool recognized as a reliable source of important levels on the chart. We have added this functionality with the option to choose how you want to generate these levels and which specific levels you want to display.

You can plot Fibonacci levels based on the Swing structure, Minor structure, previous or current day, month, and more. In total, there are 10 different options for constructing the Fibonacci grid.

Above, you can see an example of how it appears on the chart, and below you will find the settings available in this section.

🈹 Premium and Discount

Another useful feature for all traders is the Premium and Discount zones based on structure. This makes it easy to identify areas of interest—whether in a discount or premium zone, or in an equilibrium area.

Below, you can also see the settings available in this section.

✅ Additional Function

We have also separated a few functions into their own section:

Color Candles – Colors the candles according to the current trend.

Market Structure ZigZag – Visually highlights the zigzag used to form the structure.

Key Point Labels – Displays the points on the chart from which the structure is built.

Equal Highs & Lows – Identifies equal highs and lows as areas of potential liquidity for larger market players, as price often aims to sweep these zones.

Below are a few screenshots showing how these features appear on the chart.

Color Candles

Market Structure ZigZag and Key Point Labels

Equal Highs & Lows

Below, you can see a screenshot displaying all the settings available in this section.

🎨 General Styling

We have devoted considerable effort to providing flexible customization for each element on the chart, so you can design the exact look you want. That’s why we created an additional section where you can adjust any element’s size, style, and more.

Combined with extensive color and transparency options, this feature provides a flexible appearance for the indicator on any chart.

Below, you can see the settings available in this section

🔔 Alert Customization

You can configure over 16 types of reactions to various events on the chart. Additionally, you can set up alerts to trigger at specific fill levels and explore numerous other alert options, as shown in the screenshot below.

🟠 Usage Examples

We have also prepared several examples of how to use the indicator. These are standard entry models taken from the classic Smart Money concept.

First Example

In the screenshot above, the market displays a downward structure until a manipulation occurs, followed by a CHoCH break. This is a standard entry model featuring an entry at the nearest FVG, a stop-loss placed beyond the manipulation, and a target at the nearest liquidity zone—whether session-based or, as in our case, a gap (one of the FVG types) that price commonly revisits.

This is considered a more aggressive entry because we only waited for a single confirmation of the trend change—the CHoCH break—and then entered immediately afterward. While the WinRate might be lower in such trades, the Risk-Reward ratio is typically very high if you correctly identify the manipulation.

Second Example

This approach is more conservative and less risky, typically offering a higher WinRate but with a lower Risk-Reward ratio.

Here, we use the 4H FVG as our decision point (POI). With the indicator, we plot the 4-hour FVG on our current chart without needing to switch back and forth between timeframes.

Once price reaches our POI, we look for an entry model that includes three confirmations:

First Confirmation – A CHoCH break.

Second Confirmation – A manipulation.

Third Confirmation – A second BOS break.

We wait for all these confirmations before entering the trade, ensuring our stop-loss is well-protected since the remaining liquidity has been swept and the 4-hour FVG has been fully filled.

Our target is the full fill of a higher timeframe FVG or other high-liquidity levels below.

In a conservative setup, it is crucial to allow a complete OrderFlow to develop, including manipulations and clear breaks of lower levels. This approach helps protect the trade and often results in a higher WinRate.

🟠 Disclaimer

Past performance is not indicative of future results. To trade successfully, it is crucial to have a thorough understanding of the market context and the specific situation at hand. Always conduct your own research and analysis before making any trading decisions.

To gain access to the indicator, please review the author's instructions below this post

Pesquisar nos scripts por "high low"

[TA] Breaker BlocksDescription:

The Breaker Blocks Finder is a sophisticated tool designed for traders who seek to identify key market structures algorithmically. This indicator meticulously scans for both bullish and bearish breaker blocks, visually delineating them on the chart for easy identification.

Exploring ICT Breaker Blocks: Enhancing Your Trading with Precision

Understanding ICT Breaker Blocks: ICT Breaker Blocks are a nuanced trading concept that leverages market liquidity and manipulation to identify potential breakout points. This strategy is particularly effective in pinpointing moments where the market is poised for a significant directional move.

Mechanics of ICT Breaker Blocks: The essence of this strategy lies in detecting manipulation phases where liquidity is being accumulated, typically around critical market highs or lows. This setup leads to a Stop Hunt, a tactical move to trigger stop orders and fuel a breakout in the opposite direction.

Detailed Breakdown of Breaker Block Types:

Bullish Breaker Blocks:

• Bullish Order Block: The precursor to a bullish breakout, setting the stage for a potential upward move.

• Bullish Breaker Candle: An upward-closing candle that forms just before breaking past an old low, signaling a bullish reversal.

• Confirmation: Achieved when the price dips below the prior low and subsequently rises above the high of the swing, solidifying the bullish breakout.

• Identification: Look for a failed bearish order block, indicated by an initial drop in prices that ultimately reverses, hinting at a bullish shift.

• Key Elements: Monitor the pattern of lows and highs (low, high, lower low, higher high), which suggests an emerging bullish trend.

Bearish Breaker Blocks:

• Bearish Breaker Candle: A downward-closing candle that appears right before an old high is surpassed, indicating a bearish reversal.

• Confirmation: Occurs when prices climb above the previous high and then descend below the swing's low, confirming the bearish move.

• Identification: Initiate by identifying a failed bullish order block, where initial upward price momentum falters and reverses, signaling bearish potential.

• Key Elements: Focus on the sequence of highs and lows (high, low, higher high, lower low), which may denote a looming bearish trend.

Spotting High Probability Breaker Blocks: To enhance the reliability of breaker block identification, incorporate patterns that exhibit a Fair Value Gap (FVG), which typically indicates a stronger likelihood of a successful breakout.

Leveraging ICT Breaker Blocks in Trading: Our Inner Circle Trading mentorship delves into these concepts and more, providing you with comprehensive education and weekly market insights.

By mastering ICT Breaker Blocks, you're equipped with a powerful tool to navigate the intricacies of the market, making informed and strategic trading decisions.

This channel provides you with comprehensive education and weekly market insights. If you enjoyed this thread, like, share, and follow. Join us for an in-depth exploration of advanced trading strategies, and elevate your trading proficiency.

Still confused about Breaker Blocks?

Follow these steps for Bullish Breaker Blocks and reverse them for Bearish Breaker Blocks.

Think:

Bullish BB = Low, High, Lower Low, then Higher High

Bearish BB = High, Low, Higher High, then Lower Low

While this tool is a powerful addition to your trading strategy, it's important to note that it is not an autotrader. Traders should use this indicator as part of a comprehensive trading plan, considering other market factors and personal risk tolerance.

Risk Disclaimer:

Trading financial markets involves significant risk and can result in the loss of your invested capital. You should not invest more than you can afford to lose and should ensure that you fully understand the risks involved. Before trading, please take into consideration your level of experience, investment objectives, and seek independent financial advice if necessary. This indicator is provided as-is without any guarantees or warranty. Use of this indicator is at your own risk, and the creator is not responsible for any financial losses or damages.

Trading Range FinderThere are 5 horizontal lines printed by this indicator, and they extend from the last bar to a user-defined look-back period (the number of bars back from the last bar). The dark blue lines are the swing high and swing low within the look-back period. The magenta lines are the range high and range low used to define a trading range for the look-back period. The light blue line in the middle is the halfway point within the trading range, or the equilibrium.

The majority of the script logic focuses on the placement of the magenta lines (range high and range low). To do this, a histogram analysis is used. The price difference between the swing high and swing low is broken up into discrete bins which are monitored by an array. The high and low of each bar within the look-back period is used to populate the bins. There is also a toggle to use the midpoint of each bar to populate the bins as well. This means that for every bar two bins (three with the toggle) within the array will increase by a value of 1. The two bins with the highest count are used to print the magenta lines. Around each magenta line are two dotted lines and a shaded area to show the size of the bins used in the analysis.

Regarding bin size:

The bin size is a fraction of the asset price. If the price difference between the swing high and swing low is $1000, and the bin size is 1, then there are 1000 bins. I initially made the bin size a user input, but for a given look-back period the trading range would have wildly different range highs/lows when the bin size was incremented by small amounts. It was also difficult to manage a user input when the asset price is near, or less than 1. I then used a loop to optimize the bin size so it is no longer a user input. The optimization parameter is the maximization of the distance between the range high and range low. I capped the bin size within the script somewhat arbitrarily (but with a lot of testing) at ((swing high - swing low)/50) because sometimes very large bin sizes (one third or one quarter of the difference between swing high and swing low) would maximize the distance between the range high and range low, but with the line placed in the middle of the bin, its level wouldn't always make sense. Besides the maximum bin size, the only other hardcoded part of the script was to test 50 bin sizes, up to and including the maximum bin size. The loop finds the bin size that gives the largest separation between prices, and then uses that bin size to set the up the array with the bin counts.

Toggles for the plots are available to show how the range high, range low, and equilibrium move as new bars are added to the chart. The effects of these plots can most readily be seen in replay mode. There is also to a toggle to show the Fibonacci levels between the range high and range low. I made the midpoint a toggle because sometimes it is detrimental, meaning it contracts the trading range to the point of not being useful on a given chart. If there are periods of very low volatility and the bin size is large enough, the midpoint might end up in the same bin as the high or the low (or both!), and a single bar could unevenly weight a particular bin. The midpoint toggle, along with different lookback periods, will be needed to find a suitable trading range for a given chart.

Price-Action CandlesWhat is a swing high or swing low?

Swing highs and lows are price extremes. For example say we set our swing length to 5. A candle that is a swing high with a swing length of 5 will have 5 bars to the left that are lower and 5 bars to the right that are lower. A candle that is a swing low with a swing length of 5 will have 5 bars to the left that are higher and 5 bars to the right that are higher.

How are the trend candles calculated?

The trend candles are calculated by storing and comparing historical swing lows and swing highs.

The pinescript code goes as follows:

The pinescript code goes as follows:

var int trend = na

trend := ((hh and high >= psh) or close > csh) ? 1 : ((ll and low <= psl) or close < csl) ? -1 : lh or hl ? 0 : trend

What does that gibberish mean?

-Candle can be GREEN IF

- We have a higher high (current swing high is greater than the previous swing high) and the high is greater than the previous swing high

- OR The current close is greater than the current swing high

-Candle can be RED IF

- We have a lower low (current swing low is less than the previous swing low) and the low is less than the previous swing low

- OR The current close is less than the current swing low

-Candle can be YELLOW IF

- We have a new swing high and the new swing high is less than the previous swing high

- OR We have a new swing low and the new swing low is greater than the previous swing low

If none of the conditions above are true then we continue with whatever color the previous bar was.

What is repainting?

Repainting is "script behavior causing historical vs realtime calculations or plots to behave differently." That definition comes directly from Tradingview. If you want to read the full explanation you can visit it here www.tradingview.com . The price-action candles use swing highs and swing lows which need bars to the left (past) and bars to the right ("future") in order to confirm the swing level. Because of the need to wait for confirmation to for swing levels the plot style can be repainting. With the price-action candles indicator the only repainting part of the indicator is the labels. The price-action candles themselves WILL NOT REPAINT. The labels however can be set to repaint or not depending on the user preference. If the user opts to use repainting then the label location is shifted back by the length of the price-action. So if the "Price-Action Length" input is set to 10, and the user wants repainting, the swing high/low label will be shifted back 10 bars. If the user opts for no repainting, the label will not be shifted and instead show on the exact bar the swing level was confirmed.

Examples Below.

Repaint

Here the labels are shifted back the price-action length.

Non-Repaint

Here the labels are not shifted back because the input setting is set to not repaint.

Multi-timeframe Analysis

The users can view the trend from multiple different timeframes at once with a table displayed at the bottom of their charts. The timeframe can be lower or higher than the chart timeframe.

More examples

Be on the lookout for the Price Action Candles (Lower) indicator where you can view the multi-timeframe labels on a lower price grid in order to see the history over time!

Liquidity composition / quantifytools- Overview

Liquidity composition divides each candle into sections that are used to display transaction activity at price. In simple terms, an X-ray through candle is formed, revealing the orderflow that built the candle in greater detail. Liquidity composition consists of two main components, lots and columns. Lots and columns can be used to visualize user specified volume types, currently supporting net volume and volume delta. Lots and columns can be used to visualize same or different volume types, allowing a combination of volume footprint, volume delta footprint and volume profile in one single view. Liquidity composition principally works on any chart, whether that is equities, currencies, cryptocurrencies or commodities, even charts with no volume data (in which case volatility is used to approximate transaction activity). The script also works on any timeframe, from minute charts to monthly charts. Orderflow can be observed in real-time as it develops and none of the indications are repainted.

Example: Displaying same volume types on lots and columns

Example: Displaying different volume types on lots and columns

Liquidity composition supports user specified derivative data, such as point of control(s) and net activity coloring. Derivative data can be calculated based on either net volume or volume delta, resulting in different highlights.

With net volume, volume delta and derivative data in one view, key orderflow events such as delta imbalances, high volume nodes, low volume nodes and point of controls can be used to quickly identify accumulation/distribution, imbalances, unfinished/finished auctions and trapped traders.

Accessing script 🔑

See "Author's instructions" section, found at bottom of the script page.

Key takeaways

- Liquidity composition breaks down transaction activity at price, measured in net volume or volume delta

- Developing activity can be observed real-time, none of the indications are repainted

- Transaction activity is calculated using volumes accrued in lower timeframe price movements

- Lots and columns can be used to display same or different volume types (e.g. volume delta lots and net volume columns) in single view

- Users can specify derivative data such as volume delta POCs, net volume POC and net activity coloring

- For practical guide with practical examples, see last section

Disclaimer

Orderflow data is estimated using lower timeframe price movement. While accurate and useful, it's important to note the calculations are estimations and are not based on orderbook data. Estimates are calculated by allotting volume developing on lower timeframe chart to its respective section based on closing price. Volume delta (difference between buyers/sellers) is calculated by subtracting down move volumes (sell volume) from up move volumes (buy volume). Accuracy of the orderflow estimations largely depends on quality of lower timeframe chart used for calculations, which is why this tool cannot be expected to work accurately on illiquid charts with broken data.

Liquidity composition does not provide a standalone trading strategy or financial advice. It also does not substitute knowing how to trade. Example charts and ideas shown for use cases are textbook examples under ideal conditions, not guaranteed to repeat as they are presented. Liquidity composition should be viewed as one tool providing one kind of evidence, to be used in conjunction with other means of analysis.

- Example charts

Chart #1: BTCUSDT

Chart #2: EURUSD

Chart #3: ES futures

- Calculations

By default, size of sections and lower timeframe accuracy are automatically determined for all charts and timeframes. Number of lower timeframe price moves used for calculating orderflow is kept at fixed value, by default set to 350. Accuracy value dictates how many lower timeframe candles are included in the calculation of volume at price. At 350, the script will always use 350 lower timeframe price movements in calculations (when possible). When calculated dynamic timeframe is less than 1 minute, the script switches to available seconds based timeframes. Minimum dynamic timeframe can be capped to 1 minute (as seconds based timeframes are not available for all plans) or dynamic timeframe can be overridden using an user specified timeframe.

Example: Calculating dynamic lower timeframe

Main chart: 4H / 240 minutes

Accuracy value: 100

Formula: 240 minutes / 100 = 2.4 minutes

Timeframe used for calculations = 2 minutes

Section size is automatically determined based on typical historical candle range, the bigger it is, the bigger the section size as well. Like dynamic timeframe, automatic section size can be manually overridden by user specified size expressed in ticks (minimum price unit). Users can also adjust sensitivity of automatic sizing by setting it higher (smaller sections, more detail and more noise) or lower (less sections, less detail and less noise). Section size and dynamic timeframe can be monitored via metric table.

Volume at price is calculated by allotting volume associated with a lower timeframe price movement to its respective section based on closing price (volume is stored to the section that covers closing price). When used on a chart with no volume data, volatility is used instead to determine likely magnitude of participation. Volume delta (difference between buyers/sellers) is calculated by subtracting down move volumes (sell volume) from up move volumes (buy volume). Volumes accrued in sections are monitored over a longer period of time to determine a "normal" amount of activity, which is then used to normalize accrued volumes by benchmarking them against historical values.

Volume values displayed on the left side represent how close or far volume traded at given section is to an extreme, represented by value of 10 . The more value exceeds 10, the more extreme transaction activity is historically. The lesser the value, the less extreme (and therefore more typical) transaction activity is. Users can adjust sensitivity of volume extreme threshold, either by increasing it (more transaction activity is needed to constitute an extreme) or decreasing it (less transaction activity is needed to constitute an extreme).

Example: Interpreting volume scale

0 = Very little to no transaction activity compared to historical values

5 = Transaction activity equal to average historical values

10 = Transaction activity equal to an extreme in historical values

10+ = The more transaction activity exceeds value of 10, the more extreme it is historically

Accuracy of orderflow data largely depends on quality of lower timeframe data used in calculations. Sometimes quality of underlying lower timeframe data is insufficient due to suboptimal accuracy or broken lower timeframe data, usually caused by illiquid charts with gaps and inconsistent values. Therefore, one should always ensure the usage of most liquid chart available with no gaps in lower timeframe data. To combat poor orderflow data, a simple data quality check is conducted by calculating percentage of sections with volume data out of all available sections. Idea behind the test is to capture instances where unusual amount of sections are completely empty, most likely due to data gaps in LTF chart. E.g. 90% of sections hold some volume data, 10% are completely empty = 90% data quality score.

Data quality score should be viewed as a metric alerting when detail of underlying data is insufficient to consider accurate. When data quality score is slightly below threshold, lower timeframe chart used for calculations is likely fine, but accuracy value is too low. In this case, one should increase accuracy value or manually override used timeframe with a smaller one. When data quality score is well below threshold, lower timeframe chart used for calculations is likely broken and cannot be fixed. In this case, one should look for alternative charts with more reliable data (e.g. ES1! -> SPY, BITSTAMP:BTCUSD -> BINANCE:BTCUSDT).

Example : When insufficient data quality scores can/cannot be fixed

- Derivative data

Point of control

Point of control, referring to point in price where transaction activity is highest, can be calculated based on the volume type of lots or columns (based on net volume or volume delta). Depending on the calculation basis, displayed point of controls will vary. POC calculated based on net volume is no different from traditional POC, it is simply the section with highest amount of transaction activity, marked with an X. When calculating POC based on volume delta, the script will highlight two point of controls, named leading and losing point of control . Leading POC refers to lot with highest amount of volume delta, marked with an X. If leading POC was net buy volume, losing POC is marked on section with highest net sell volume, marked with S respectfully. Same logic applies in vice versa, if leading POC is net sell volume, losing POC is marked on highest buy volume section, using the letter B.

Net activity

Similarly to point of control calculation, net activity can be calculated based on either volume types, lots or columns. When calculating net activity based on net volume, candles will be colorized according to magnitude of total volume traded. When calculating net activity based on volume delta, candles will be colorized according to side with most volume traded (buyers or sellers). Net activity color can be applied on borders or body of a candle.

- Visuals

Lots, columns, candles and POCs can be colorized using a fixed color or a volume based dynamic color, with separate color options for buy side volume, sell side volume and net volume.

Metric table can be offsetted horizontally or vertically from any four corners of the chart, allowing space for tables from other scripts.

Table sizes, label sizes and offsets for visuals are fully customizable using settings menu.

- Practical guide

OHLC data (candles) is a simple condensed visualization of an auction market process. Candles show where price was in the beginning of an auction period (timeframe), the highest/lowest point and where price was at the end of an auction. The core utility of Liquidity composition is being able to view the same auction market process in much greater detail, revealing likely intention, effort and magnitude driving the process. All basic orderflow concepts, such as ones presented by auction market theory can be applied to Liquidity composition as well.

The most obvious and easy to spot use case for orderflow tools is identifying trapped traders/absorption, seen in high transaction activity at the very highs/lows of a candle or even better, at wicks. High participation at wicks can be used to identify forced orders absorbed into limit orders, idea behind being that when high transaction activity is placed at a wick, price went one direction with a lot of participation (high effort) and came right back up (low impact) within the same time period.

Absorption can show itself in many ways:

- Extreme buy volume sections at wick highs or buy side POC at wick highs

- Multiple, clustered high buy volume sections (but not extreme) at wick highs

- Positive net volume delta into a reversal down

- Extreme sell volume sections at wick lows or sell side POC at wick lows

- Multiple, clustered high sell volume sections (but not extreme) at wick lows

- Negative net volume delta into a reversal up

- Extreme net volume sections at or net volume POC at wick highs/lows

- Extreme net volume into a reversal up/down

For accurate analysis, orderflow based events should be viewed in the context of price action. To identify absorption, it's best to look for opportunities where an opposing trend is clearly in place, e.g. absorption into highs on an uptrend, absorption into lows on a downtrend. When price is ranging without a clear trend or there's no opposing trend, extreme activity at an extreme end of a candle might be aggressive participants attempting to initiate a new trend, rather than getting absorbed in the same sense. With enough effort put into pushing price to the opposite direction at overextended price, a shift in trend direction might be near.

Price action based levels are a great way to get context around orderflow events. Simple range highs/lows as a single data point serve as a high probability regimes for reversals, making them a great point of confluence for identifying trapped traders.

Low to zero volume sections can be used to identify points in price with little to no trading, leaving a volume null/void behind. Typically sections like these represent gaps on a lower timeframe chart, which can be used as reference levels for targets and support/resistance.

Net volume can be used for same purposes as above, but for determining general intention of market participants it's a much more suitable tool than volume delta. According to auction market theory, low/no participation is considered to reject prices and high participation is considered to accept prices. With this concept in mind, unfinished auctions occur when participation is high at highs or high at lows, idea behind being that participants are showing willingness and interest to trade at higher or lower prices. Auction is considered finished when the opposite is true, i.e. when participants are not showing willingness to trade at higher/lower prices. In general, direction of unfinished auctions can be expected to continue shortly and direction of unfinished auctions can be expected to hold.

While shape of volume delta and net volume are usually similar, they're not the same thing and do not represent the same event under the hood. Volume delta at 0 does not necessarily mean participation is 0, but can also mean high participation with equal amount of buying and selling. With this distinction in mind, using volume delta and net volume in tandem has the benefit of being able to identify points in price with a lot of up and down price movement packed into a small area, i.e. consolidation. Points in price where price hangs around for an extended period of time can be used to identify levels of interest for re-tests and breakout opportunities.

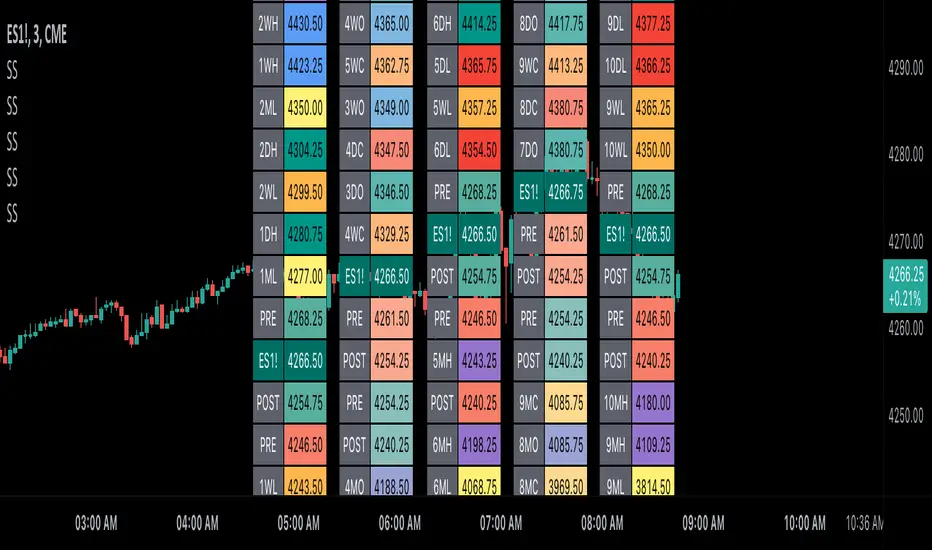

Scoopy StacksWaffle Around Multiple

(Open, High, Low, Close) Stacks On

Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Columns, Rows, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Stacks.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 STACKS:

Default Value: (1)

Incremental Stack Value, Increasing Value

Swaps Sessions With the Next Two Stacks

(✓) Swap Stacks?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Stacks?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Stack:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Stack Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Stack Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Stack Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Stack Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Stack Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Stack Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Stack Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Stack Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 TABLES:

Default Value: (1)

Moves Table Up, Down, Left, or Right

Based on Second Default Value

First Default Value: (Top Right)

Sets Table Placement, Middle Center

Allows Table To Move In All Directions

Second Default Value: (Default)

Fixed Table Position, Switching Values

Moves Direction of the Table

🟦 IDEAS:

(✓) Show Ideas?

Shows Four Ideas With Custom Texts

and Values; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥇)

Shown On First Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥈)

Shown On Second Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥉)

Shown On Third Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🎖️)

Shown On Fourth Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

Ribbit RangesBounce Around Multiple

(Open, High, Low, Close) Ranges

On Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Lines, Labels, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Ranges.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 RANGES:

Default Value: (1)

Incremental Range Value, Increasing Value

Swaps Sessions With the Next Two Ranges

(✓) Swap Ranges?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Ranges?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Range:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Range Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Range Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Range Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Range Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Range Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Range Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Range Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Range Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 COLORS:

(✓) Swap Colors?

Text Color Is Shown Using

Background Color

( ) Swap Colors?

Background Color Is Shown

Using Text Color

🟦 IDEAS:

(✓) Show Ideas?

Plots Four Ideas With Custom Lines

and Labels; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥇)

Shown On First Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥈)

Shown On Second Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥉)

Shown On Third Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🎖️)

Shown On Fourth Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

Z-Score Based Momentum Zones with Advanced Volatility ChannelsThe indicator "Z-Score Based Momentum Zones with Advanced Volatility Channels" combines various technical analysis components, including volatility, price changes, and volume correction, to calculate Z-Scores and determine momentum zones and provide a visual representation of price movements and volatility based on multi timeframe highest high and lowest low values.

Note: THIS IS A IMPROVEMNT OF "Multi Time Frame Composite Bands" INDICATOR OF MINE WITH MORE EMPHASIS ON MOMENTUM ZONES CALULATED BASED ON Z-SCORES

Input Options

look_back_length: This input specifies the look-back period for calculating intraday volatility. correction It is set to a default value of 5.

lookback_period: This input sets the look-back period for calculating relative price change. The default value is 5.

zscore_period: This input determines the look-back period for calculating the Z-Score. The default value is 500.

avgZscore_length: This input defines the length of the momentum block used in calculations, with a default value of 14.

include_vc: This is a boolean input that, if set to true, enables volume correction in the calculations. By default, it is set to false.

1. Volatility Bands (Composite High and Low):

Composite High and Low: These are calculated by combining different moving averages of the high prices (high) and low prices (low). Specifically:

a_high and a_low are calculated as the average of the highest (ta.highest) and lowest (ta.lowest) high and low prices over various look-back periods (5, 8, 13, 21, 34) to capture short and long-term trends.

b_high and b_low are calculated as the simple moving average (SMA) of the high and low prices over different look-back periods (5, 8, 13) to smooth out the trends.

high_c and low_c are obtained by averaging a_high with b_high and a_low with b_low respectively.

IDV Correction Calulation : In this script the Intraday Volatility (IDV) is calculated as the simple moving average (SMA) of the daily high-low price range divided by the closing price. This measures how much the price fluctuates in a given period.

Composite High and Low with Volatility: The final c_high and c_low values are obtained by adjusting high_c and low_c with the calculated intraday volatility (IDV). These values are used to create the "Composite High" and "Composite Low" plots.

Composite High and Low with Volatility Correction: The final c_high and c_low values are obtained by adjusting high_c and low_c with the calculated intraday volatility (IDV). These values are used to create the "Composite High" and "Composite Low" plots.

2. Momentum Blocks Based on Z-Score:

Relative Price Change (RPC):

The Relative Price Change (rpdev) is calculated as the difference between the current high-low-close average (hlc3) and the previous simple moving average (psma_hlc3) of the same quantity. This measures the change in price over time.

Additionally, std_hlc3 is calculated as the standard deviation of the hlc3 values over a specified look-back period. The standard deviation quantifies the dispersion or volatility in the price data.

The rpdev is then divided by the std_hlc3 to normalize the price change by the volatility. This normalization ensures that the price change is expressed in terms of standard deviations, which is a common practice in quantitative analysis.

Essentially, the rpdev represents how many standard deviations the current price is away from the previous moving average.

Volume Correction (VC): If the include_vc input is set to true, volume correction is applied by dividing the trading volume by the previous simple moving average of the volume (psma_volume). This accounts for changes in trading activity.

Volume Corrected Relative Price Change (VCRPD): The vcrpd is calculated by multiplying the rpdev by the volume correction factor (vc). This incorporates both price changes and volume data.

Z-Scores: The Z-scores are calculated by taking the difference between the vcrpd and the mean (mean_vcrpd) and then dividing it by the standard deviation (stddev_vcrpd). Z-scores measure how many standard deviations a value is away from the mean. They help identify whether a value is unusually high or low compared to its historical distribution.

Momentum Blocks: The "Momentum Blocks" are essentially derived from the Z-scores (avgZScore). The script assigns different colors to the "Fill Area" based on predefined Z-score ranges. These colored areas represent different momentum zones:

Positive Z-scores indicate bullish momentum, and different shades of green are used to fill the area.

Negative Z-scores indicate bearish momentum, and different shades of red are used.

Z-scores near zero (between -0.25 and 0.25) suggest neutrality, and a yellow color is used.

Moving Average - TREND POWER v1.1- (AS)0)NOTE:

This is first version of this indicator. It's way more complicated than it should be. Check out Moving Average-TREND POWER v2.1-(AS), its waaaaay less complicated and might be better.Enjoy...

1)INTRODUCTION/MAIN IDEA:

In simpliest form this script is a trend indicator that rises if Moving average if below price or falling if above and going back to zero if there is a crossover with a price. To use this indicator you will have to adjust settings of MAs and choose conditions for calculation.

While using the indicator we might have to define CROSS types or which MAs to use. List of what cross types are defined in the script and Conditiones to choose from.The list will be below.

2) COMPOSITION:

-MA1 can be defined by user in settings, possible types: SMA, EMA, RMA, HMA, TEMA, DEMA, LSMA, WMA.

-MA2 is always ALMA

3) OVERLAY:

Default is false but if you want to see MA1/2 on chart you can change code to true and then turn on overlay in settings. Most plot settings are avalible only in OV=false.

if OV=true possible plots ->MA1/2, plotshape when choosen cross type

if OV=false -> main indicator,TSHs,Cross counter

4)PRESETS :

Indicator has three modes that can be selected in settings. First two are presets and do not require selecting conditions as they set be default.

-SIMPLE - most basic

-ABSOLUTE - shows only positive values when market is trending or zero when in range

-CUSTOM - main and the most advanced form that will require setting conditions to use in calculating trend

4.1)SIMPLE – this is the most basic form of conditions that uses only First MA. If MA1 is below selected source (High/Low(High for Uptrend and Low for DNtrend or OHLC4) on every bar value rises by 0.02. if it above Low or OHLC4 it falls by 0.02 with every bar. If there is a cross of MA with price value is zero. This preset uses CROSS_1_ULT(list of all cross types below)

4.2) ABSOLUTE – does not show direction of the trend unlike others and uses both MA1 and MA2. Uses CROSS type 123_ULT

4.3) CUSTOM – here we define conditions manually. This mode is defined in parts (5-8 of description)

5)SETTINGS:

SOURCE/OVERLAY(line1) – select source of calculation form MA1/MA2, select for overlay true (look point 3)

TRESHOLDS(line2). – set upper and lower THS, turn TSHs on/off

MA1(line3) – Length/type of MA/Offset(only if MA type is LSM)

MA2(line4) – length/offset/sigma -(remember to set ma in the way that in Uptrend MA2MA1 in DNtrend)

Use faster MA types for short term trends and slower types / bigger periods for longer term trends, defval MA1/2 settings

are pretty much random so using them is not recomended.

CROSSshape(line5) – choose which cross type you want to plot on chart(only in OV=true) or what type you want to use in counting via for loops,

CROSScount(line6) – set lookback for type of cross choosen above

BOOLs in lines 5 and 6 - plotshape if OV=true/plot CROSScount histogram (if OV=false)

Lines 7 and 8 – PRESET we want to use /SRC for calculation of indicator/are conditions described below/which MAs to use/Condition for

reducing value t 0 - (if PRESET is ABSOLUTE or SIMPLE only SRC should be set(Line 8 does not matter if not CUSTOM))

5)SOURCE for CONDS:

Here you can choose between H/L and OHLC. If H/L value grow when MAlow. If OHLC MAOHLC. H/L is set by default and recommended. This can be selected for all presets not only CUSTOM

6)CROSS types LIST:

“1 means MA1, 2 is MA2 and 3 I cross of MA1/MA2. L stands for low and H for high so for example 2H means cross of MA2 and high”

NAME -DEFINITION Number of possible crosses

1L - cross of MA1 and low 1

1H - cross of MA1 and high 1

1HL - cross of MA1 and low or MA1 and high 2 -1L/1H

2L - cross of MA2 and low 1

2H - cross of MA2 and high 1

2HL - cross of MA2 and low or MA1 and high 2 -2L/2H

12L - cross of MA1 and low or MA2 and low 2 -1L/2L

12H - cross of MA1 and high or MA2 and high 2 -1H/2H

12HL - MA1/2 and high/low 4 -1H/1L/2H/2L

3 -cross of MA1 and MA2 1

123HL -crosses from 12HL or 3 5 -12HL/3

1_ULT - cross of MA1 with any of price sources(close,low,high,ohlc4 etc…)

2_ULT - cross of MA2 with any of price sources(close,low,high,ohlc4 etc…)

123_ULT – all crosses possible of MA1/2 (all of the above so a lot)

7)CRS CONDS:

“conditions to reduce value back to zero”

>/< - 0 if indicator shows Uptrend and there’s a cross with high of selected MA or 0 if in DNtrend and cross with low. Better for UP/DN trend detection

ALL – 0 if cross of MA with high or low no matter the trend, better for detecting consolidation

ULT – if any cross of selected MA, most crosses so goes to 0 most often

8)MA selection and CONDS:

-MA1: only MA1 is used,if MA1 below price value grows and the other way around

MA1price =-0.02

-MA2 – only MA2 is used, same conditions as MA1 but using MA2

MA2price =-0.02

-BOTH – MA1 and MA2 used, grows when MA1 if below, grows faster if MA1 and MA2 are below and fastest when MA1 and MA2 are below and MA2price=-0.02

-MA1 and MA2 >price=-0.03

-MA1 and MA2 ?price and MA2>MA1=-0.04

9)CONDITIONS SELECTION SUMMARRY:

So when CUSTOM we choose :

1)SOURCE – H/L or OHLC

2)MAs – MA1/MA2/BOTH

3)CRS CONDS (>/<,ALL,ULT)

So for example...

if we take MA1 and ALL value will go to zero if 1HL

if MA1 and >/< - 0 if 1L or 1H (depending if value is positive or negative).(1L or 1H)

If ALL and BOTH zero when 12HL

If BOTH and ULT value goes back to zero if Theres any cross of MA1/MA2 with price or cross of MA1 and MA2.(123_ULT)

If >/< and BOTH – 0 if 12L in DNtrend or 12H if UPtrend

10) OTHERS

-script was created on EURUSD 5M and wasn't tested on different markets

-default values of MA1/MA2 aren't optimalized so do not

-There might be a logical error in the script so let me know if you find it (most probably in 'BOTH')

-thanks to @AlifeToMake for help

-if you have any ideas to improve let me know

-there are also tooltips to help

GKD-C Adaptive-Lookback Variety RSI [Loxx]Giga Kaleidoscope GKD-C Adaptive-Lookback Variety RSI is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-C Adaptive-Lookback Variety RSI

What is the Adaptive Lookback Period?

The adaptive lookback period is a technique used in technical analysis to adjust the period of an indicator based on changes in market conditions. This technique is particularly useful in volatile or rapidly changing markets where a fixed period may not be optimal for detecting trends or signals.

The concept of the adaptive lookback period is relatively simple. By adjusting the lookback period based on changes in market conditions, traders can more accurately identify trends and signals. This can help traders to enter and exit trades at the right time and improve the profitability of their trading strategies.

The adaptive lookback period works by identifying potential swing points in the market. Once these points are identified, the lookback period is calculated based on the number of swings and a speed parameter. The swing count parameter determines the number of swings that must occur before the lookback period is adjusted. The speed parameter controls the rate at which the lookback period is adjusted, with higher values indicating a more rapid adjustment.

The adaptive lookback period can be applied to a wide range of technical indicators, including moving averages, oscillators, and trendlines. By adjusting the period of these indicators based on changes in market conditions, traders can reduce the impact of noise and false signals, leading to more profitable trades.

In summary, the adaptive lookback period is a powerful technique for traders and analysts looking to optimize their technical indicators. By adjusting the period based on changes in market conditions, traders can more accurately identify trends and signals, leading to more profitable trades. While there are various ways to implement the adaptive lookback period, the basic concept remains the same, and traders can adapt and customize the technique to suit their individual needs and trading styles.

This indicator includes 10 types of RSI

1. Regular RSI

2. Slow RSI

3. Ehlers Smoothed RSI

4. Cutler's RSI

5. Rapid RSI

6. Harris' RSI

7. RSI DEMA

8. RSI TEMA

9. RSI T3

10. Jurik RSX

Regular RSI

The Relative Strength Index (RSI) is a widely used technical indicator in the field of financial market analysis. Developed by J. Welles Wilder Jr. in 1978, the RSI is a momentum oscillator that measures the speed and change of price movements. It helps traders identify potential trend reversals, overbought, and oversold conditions in a market.

The RSI is calculated based on the average gains and losses of an asset over a specified period, typically 14 days. The formula for calculating the RSI is as follows:

RSI = 100 - (100 / (1 + RS))

Where:

RS (Relative Strength) = Average gain over the specified period / Average loss over the specified period

The RSI ranges from 0 to 100, with values above 70 generally considered overbought (potentially indicating that the asset is overvalued and may experience a price decline) and values below 30 considered oversold (potentially indicating that the asset is undervalued and may experience a price increase).

Slow RSI

Slow RSI is a modified version of the Relative Strength Index (RSI) indicator that aims to provide a smoother, more consistent signal than the traditional RSI. The Slow RSI is designed to be less sensitive to sudden price movements, which can cause false signals.

To calculate Slow RSI, we first calculate the up and down values, just like in traditional RSI and Ehlers RSI. The up and down values are calculated by comparing the current price to the previous price, and then adding up the positive and negative differences.

Next, we calculate the Slow RSI value using the formula:

SlowRSI = 100 * up / (up + dn)

where "up" and "dn" are the total positive and negative differences, respectively.

This formula is similar to the one used in traditional RSI, but the dynamic lookback period based on the average of the up and down values is used to smooth out the signal.

Finally, we apply smoothing to the Slow RSI value by taking an exponential moving average (EMA) of the Slow RSI values over a specified period. This EMA helps to reduce the impact of sudden price movements and provide a smoother, more consistent signal over time.

Ehler's Smoothed RSI

Ehlers RSI is a modified version of the Relative Strength Index (RSI) indicator created by John Ehlers, a well-known technical analyst and author. The purpose of Ehlers RSI is to reduce lag and improve the responsiveness of the traditional RSI indicator.

To calculate Ehlers RSI, we first smooth the prices by taking a weighted average of the current price and the two previous prices. This smoothing helps to reduce noise in the data and produce a more accurate signal.

Next, we calculate the up and down values differently than in traditional RSI. In traditional RSI, the up and down values are based on the difference between the current price and the previous price. In Ehlers RSI, the up and down values are based on the difference between the current price and the price two bars ago. This approach helps to reduce lag and produce a more responsive indicator.

Finally, we calculate Ehlers RSI using the formula:

EhlersRSI = 50 * (up - down) / (up + down) + 50

The result is a more timely signal that can help traders identify potential trends and reversals in the market. However, as with any technical indicator, Ehlers RSI should be used in conjunction with other analysis tools and should not be relied on as the sole basis for trading decisions.

Cutler's RSI

Cutler's RSI (Relative Strength Index) is a variation of the traditional RSI, a popular technical analysis indicator used to measure the speed and change of price movements. The main difference between Cutler's RSI and the traditional RSI is the calculation method used to smooth the data. While the traditional RSI uses an exponential moving average (EMA) to smooth the data, Cutler's RSI uses a simple moving average (SMA).

Here's the formula for Cutler's RSI:

1. Calculate the price change: Price Change = Current Price - Previous Price

2. Calculate the average gain and average loss over a specified period (usually 14 days):

If Price Change > 0, add it to the total gains.

If Price Change < 0, add the absolute value to the total losses.

3. Calculate the average gain and average loss by dividing the totals by the specified period: Average Gain = Total Gains / Period, Average Loss = Total Losses / Period

4. Calculate the Relative Strength (RS): RS = Average Gain / Average Loss

5. Calculate Cutler's RSI: Cutler's RSI = 100 - (100 / (1 + RS))

Cutler's RSI is not necessarily better than the regular RSI; it's just a different variation of the traditional RSI that uses a simple moving average (SMA) instead of an exponential moving average (EMA) quantifiedstrategies.com. The main advantage of Cutler's RSI is that it is not data length dependent, meaning it returns consistent results regardless of the length of the period, or the starting point within a data file quantifiedstrategies.com.

However, it's worth noting that Cutler's RSI does not necessarily outperform the traditional RSI. In fact, backtests reveal that Cutler's RSI is no improvement compared to Wilder's RSI quantifiedstrategies.com. Additionally, using an SMA instead of an EMA in Cutler's RSI may result in the loss of the "believed" advantage of weighting the most recent price action aaii.com.

Both Cutler's RSI and the traditional RSI can be used to identify overbought/oversold levels, support and resistance, spot divergences for possible reversals, and confirm the signals from other indicators investopedia.com. Ultimately, the choice between Cutler's RSI and the traditional RSI depends on personal preference and the specific trading strategy being employed.

Rapid RSI

Rapid RSI is a technical analysis indicator that is a modified version of the Relative Strength Index (RSI). It was developed by Andrew Cardwell and was first introduced in the October 2006 issue of Technical Analysis of Stocks & Commodities magazine.

The Rapid RSI improves upon the regular RSI by modifying the way the average gains and losses are calculated. Here's a general breakdown of the Rapid RSI calculation:

1. Calculate the upward change (when the price has increased) and the downward change (when the price has decreased) for each period.

2. Calculate the simple moving average (SMA) of the upward changes and the SMA of the downward changes over the specified period.

3. Divide the SMA of the upward changes by the SMA of the downward changes to get the relative strength (RS).

4. Calculate the Rapid RSI by transforming the relative strength (RS) into a value ranging from 0 to 100.

By using the simple moving average (SMA) instead of the slow exponential moving average (RMA) as in the regular RSI, the Rapid RSI tends to be more responsive to recent price changes. This can help traders identify overbought and oversold conditions more quickly, potentially leading to earlier entry and exit points. However, it is important to note that a faster indicator may also produce more false signals.

Harris' RSI

Harris RSI (Relative Strength Index) is a technical indicator used in financial analysis to measure the strength or weakness of a security over time. It was developed by Larry Harris in 1986 as an alternative to the traditional RSI, which measures the price change of a security over a given period.

The Harris RSI uses a slightly different formula from the traditional RSI, but it is based on the same principles. It calculates the ratio of the average gain to the average loss over a specified period, typically 14 days. The result is then plotted on a scale of 0 to 100, with high values indicating overbought conditions and low values indicating oversold conditions.

The Harris RSI is believed to be more responsive to short-term price movements than the traditional RSI, making it useful for traders who are looking for quick trading opportunities. However, like any technical indicator, it should be used in conjunction with other forms of analysis to make informed trading decisions.

The calculation of the Harris RSI involves several steps:

1. Calculate the price change over the specified period (usually 14 days) using the following formula:

Price Change = Close Price - Prior Close Price

2. Calculate the average gain and average loss over the same period, using separate formulas for each:

Average Gain = (Sum of Gains over the Period) / Period

Average Loss = (Sum of Losses over the Period) / Period

Gains are calculated as the sum of all positive price changes over the period, while losses are calculated as the sum of all negative price changes over the period.

3. Calculate the Relative Strength (RS) as the ratio of the Average Gain to the Average Loss:

RS = Average Gain / Average Loss

4. Calculate the Harris RSI using the following formula:

Harris RSI = 100 - (100 / (1 + RS))

The resulting Harris RSI value is a number between 0 and 100, which is plotted on a chart to identify overbought or oversold conditions in the security. A value above 70 is generally considered overbought, while a value below 30 is generally considered oversold.

DEMA RSI

DEMA RSI is a variation of the Relative Strength Index (RSI) technical indicator that incorporates the Double Exponential Moving Average (DEMA) for smoothing. Like the regular RSI, the DEMA RSI is a momentum oscillator used to measure the speed and change of price movements, and it ranges from 0 to 100. Readings below 30 typically indicate oversold conditions, while readings above 70 indicate overbought conditions.

The DEMA RSI aims to improve upon the regular RSI by addressing its limitations, such as lag and false signals. By using the DEMA, a more responsive and faster RSI can be achieved. Here's a general breakdown of the DEMA RSI calculation:

1. Calculate the price change for each period, as well as the absolute value of the change.

2. Apply the DEMA smoothing technique to both the price change and its absolute value, separately. This involves calculating two sets of exponential moving averages and combining them to create a double-weighted moving average with reduced lag.

3. Divide the smoothed price change by the smoothed absolute value of the price change.

4. Transform the result into a value ranging from 0 to 100 to obtain the DEMA RSI.

The DEMA RSI is considered an improvement over the regular RSI because it provides faster and more responsive signals. This can help traders identify overbought and oversold conditions more accurately and potentially avoid false signals.

In summary, the main advantages of these RSI variations over the regular RSI are their ability to reduce noise, provide smoother lines, and be more responsive to price changes. This can lead to more accurate signals and fewer false positives in different market conditions.

TEMA RSI

TEMA RSI is a variation of the Relative Strength Index (RSI) technical indicator that incorporates the Triple Exponential Moving Average (TEMA) for smoothing. Like the regular RSI, the TEMA RSI is a momentum oscillator used to measure the speed and change of price movements, and it ranges from 0 to 100. Readings below 30 typically indicate oversold conditions, while readings above 70 indicate overbought conditions.

The TEMA RSI aims to improve upon the regular RSI by addressing its limitations, such as lag and false signals. By using the TEMA, a more responsive and faster RSI can be achieved. Here's a general breakdown of the TEMA RSI calculation:

1. Calculate the price change for each period, as well as the absolute value of the change.

2. Apply the TEMA smoothing technique to both the price change and its absolute value, separately. This involves calculating two sets of exponential moving averages and combining them to create a double-weighted moving average with reduced lag.

3. Divide the smoothed price change by the smoothed absolute value of the price change.

4. Transform the result into a value ranging from 0 to 100 to obtain the TEMA RSI.

The TEMA RSI is considered an improvement over the regular RSI because it provides faster and more responsive signals. This can help traders identify overbought and oversold conditions more accurately and potentially avoid false signals.

T3 RSI

T3 RSI is a variation of the Relative Strength Index (RSI) technical indicator that incorporates the Tilson T3 for smoothing. Like the regular RSI, the T3 RSI is a momentum oscillator used to measure the speed and change of price movements, and it ranges from 0 to 100. Readings below 30 typically indicate oversold conditions, while readings above 70 indicate overbought conditions.

The T3 RSI aims to improve upon the regular RSI by addressing its limitations, such as lag and false signals. By using the T3, a more responsive and faster RSI can be achieved. Here's a general breakdown of the T3 RSI calculation:

1. Calculate the price change for each period, as well as the absolute value of the change.

2. Apply the T3 smoothing technique to both the price change and its absolute value, separately. This involves calculating two sets of exponential moving averages and combining them to create a double-weighted moving average with reduced lag.

3. Divide the smoothed price change by the smoothed absolute value of the price change.

4. Transform the result into a value ranging from 0 to 100 to obtain the T3 RSI.

The T3 RSI is considered an improvement over the regular RSI because it provides faster and more responsive signals. This can help traders identify overbought and oversold conditions more accurately and potentially avoid false signals.

Jurik RSX

The Jurik RSX is a technical indicator developed by Mark Jurik to measure the momentum and strength of price movements in financial markets, such as stocks, commodities, and currencies. It is an advanced version of the traditional Relative Strength Index (RSI), designed to offer smoother and less lagging signals compared to the standard RSI.

The main advantage of the Jurik RSX is that it provides more accurate and timely signals for traders and analysts, thanks to its improved calculation methods that reduce noise and lag in the indicator's output. This enables better decision-making when analyzing market trends and potential trading opportunities.

What is Adaptive-Lookback Variety RSI

This indicator allows the user to select from 9 different RSI types and 33 source types. The various RSI types is enhanced by injecting an adaptive lookback period into the caculation making the RSI able to adaptive to differing market conditions.

Additional Features

This indicator allows you to select from 33 source types. They are as follows:

Close

Open

High

Low

Median

Typical

Weighted

Average

Average Median Body

Trend Biased

Trend Biased (Extreme)

HA Close

HA Open

HA High

HA Low

HA Median

HA Typical

HA Weighted

HA Average

HA Average Median Body

HA Trend Biased

HA Trend Biased (Extreme)

HAB Close

HAB Open

HAB High

HAB Low

HAB Median

HAB Typical

HAB Weighted

HAB Average

HAB Average Median Body

HAB Trend Biased

HAB Trend Biased (Extreme)

What are Heiken Ashi "better" candles?